This is an automated archive made by the Lemmit Bot.

The original was posted on /r/machinelearning by /u/apaxapax on 2024-10-19 15:19:49+00:00.

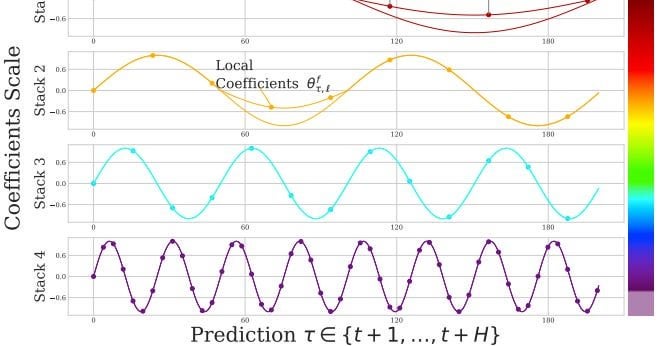

NHITs is a SOTA DL for time-series forecasting because:

- Accepts past observations, future known inputs, and static exogenous variables.

- Uses multi-rate signal sampling strategy to capture complex frequency patterns — essential for areas like financial forecasting.

- Point and probabilistic forecasting.

You can find a detailed analysis of the model here:

You must log in or register to comment.